Click on image at left for printer-friendly version

Click on image at left for printer-friendly version

By David R. Hines, CFA, Director of Research

The downside of bull markets is that our expected future returns decline as prices rise. Today, our expected returns suggest investors confront a low return landscape across most asset classes. As expected future returns fall, investors look for ways to boost returns in their portfolios. To this end, many are asking questions about the return-enhancing potential of “alternative” asset classes.

Alternative asset classes include investments in equities, bonds, private equity/debt, real estate, etc. We have spent a considerable amount of our research time searching for suitable alternative asset classes. In this note we will update you with our findings thus far.

Alternatives Haven’t Performed

Investors faced a similar, low expected returns landscape in the middle of the last decade as the S&P 500 rose thru the middle of 2007. They looked beyond conventional asset classes for ways to engineer higher returns. There was a rush to add alternative investments, especially by institutional investors. Most of these strategies promised higher returns with lower risk. Many institutional investors reworked their strategic asset allocations to increase alternative investments. As a consequence, they reduced their core stocks and bond allocations. Money poured into hedge funds, private equity, and other investment products deemed “alternatives”.

A significant amount of time has passed since these fund flows found their way into alternatives so we can now begin to evaluate the investment results. Admittedly, analyzing alternatives investment results can be difficult. There is no single definition of “alternatives” because the asset class includes a wide variety of mandates. We therefore do not focus on a single benchmark; instead, we reviewed a variety of sources to see if alternatives have lived up to their performance promise.

We begin with a famous wager Warren Buffett made six years ago. He made a bet with a New York investment consulting firm that a low fee stock index fund could beat a portfolio of high priced hedge funds over the next 10 years. A recent Fortune article reports on the results so far. Warren Buffett’s pick, the Vanguard 500 index fund, is up 43.8%. The portfolio of hedge funds is up 12.5%. The Oracle has a commanding lead with four years to go.

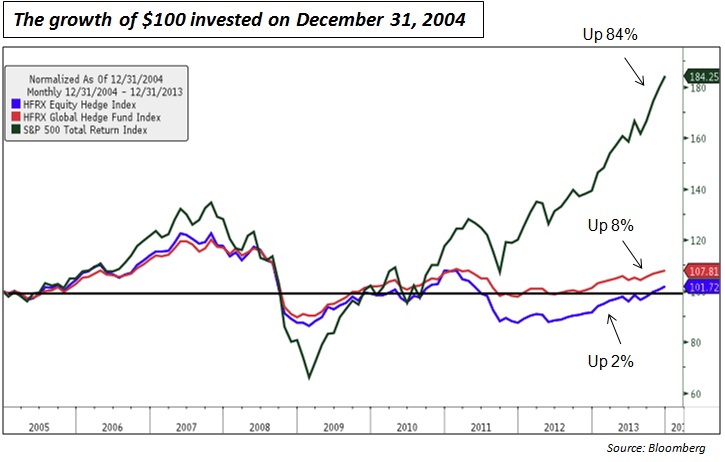

Hedge Fund Research, Inc. maintains a group of commonly used benchmarks for a variety of hedge fund strategies. We compare the return results for two indices versus the S&P 500 over the past nine years (see chart).

Hedge Fund Research, Inc. maintains a group of commonly used benchmarks for a variety of hedge fund strategies. We compare the return results for two indices versus the S&P 500 over the past nine years (see chart).

The HFRI Equity Hedge Index represents a comprehensive list of equity hedge funds. We also include the HFRI Global Hedge Index. It represents all representative hedge fund strategies. The results are even more dramatic than Warren Buffett’s simple bet. As a group, high-fee equity hedge funds are up less than 2% over the past nine years while the S&P 500 is up 84%. Global hedge funds have not fared much better. They trailed the S&P 500 by 76% over the same period!

A Google search on hedge fund performance returns dozens of recent articles about poor alternative investment performance. Many of these articles use different benchmarks but come to the same conclusion. Most investors would have been better off over the past nine years in a simple 70% equity/30% bond asset allocation, which returned an impressive 66%.

Our Skeptical View

We recognize academics might argue that our performance comparisons are not “apples to apples.” Going beyond the question of their poor relative performance, we address many of the arguments often made in favor of including alternatives in portfolios.

Alternatives Provide Higher Returns

From the evidence we’ve collected, in the aggregate alternatives have not only failed to deliver high relative returns versus most conventional benchmarks, they have produced lackluster absolute returns. In fact, the HFRI Equity Index has not even kept up with inflation!

Alternatives Reduce Volatility

Large institutional investors and consultants spend vast resources finding new ways to dampen volatility in portfolios. The reason for this is they are trying to find the Holy Grail of investing – high returns with low volatility. As one can see from the chart, hedge funds generally did dampen volatility during this time period.

However, since most endowments, trusts, and foundations have a very long-term time horizon, strategies designed to reduce volatility don’t make much sense. If you have a long time horizon, volatility is not as big a risk as spending shortfall. Over the past nine years the HFRI hedge fund indexes have not protected long-term investors against inflation. Hedge funds as a group failed in protecting their investors from declining real spending/purchasing power.

Alternatives Reduce Correlation

This is a financial industry term for “diversification.” Our view on diversification is that it works well if you pay the right price for an asset. Putting an expensive asset in the portfolio just for the sake of diversification does not make sense. Expensive asset classes will at some point perform poorly.

Historical correlation relationships break down during times of extreme market stress. Stressful events happen much more frequently than finance theory might suggest. In the financial crisis of 2008/2009, correlations among asset classes increased to the point where almost everything but Treasury securities dropped in value. Just when you need diversification the most, it often fails.

Alternatives Can Hedge Specific Risks

Hedging inflation risk is an example of the justification for adding alternatives. Investors often include funds that invest in hard assets for an inflation hedge. An analysis of hedging against inflation is beyond the scope of this note; however, many well-researched studies show a portfolio of high quality equities is one of the best ways to hedge against inflation. Investors do not need to invest in high fee, exotic funds to get the best inflation protection.

Alternatives Appear Sophisticated

High fees and poor performance are a hefty price to pay to be on the other side of the velvet ropes!

Portfolio Conclusions

Certainly, we’re not condemning all alternatives. But, picking the right alternative fund is like picking a good company or bond. We remind ourselves, however, of an immutable law of investing: no asset class can deliver high returns if the price and/or fee is too high! There are no silver bullets in investing.

The heart of our investment process is to buy high quality cash flows at prices that make sense. If we can identify an investment with these characteristics within something labeled “alternative,” we would consider it for our clients. Thus far, we have found plenty of reasonably priced cash flow yields and earned strong returns from our investments in the public equity markets; and, we have done so without charging our clients the exorbitant fees many hedge funds demand.

Market Log- March 12, 2014

S&P 500: 1,868.20

10 year T-Note: 2.73%

Crude Oil: $98.11

Gold: $1,367.80

If you have questions or comments regarding this or any other communication from us, please email us at hmpresearch@hmpayson.com.

This commentary is prepared by H.M. Payson for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of H.M. Payson as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings or market sectors, but as an illustration of broader themes. H.M. Payson cannot assure that the type of investments discussed herein will outperform any other investment strategy in the future, nor can it guarantee that such investments will present the best or an attractive risk-adjusted investment in the future. Although information has been obtained from and is based upon sources H.M. Payson believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. Registration with the SEC or with any state securities authority does not imply a certain level of skill or training. All Content © 2014 HM Payson

In the face of elevated stock market volatility, rising US-China trade tensions,…

Maine Huts & Trails provides outdoor excursions in beautiful Western Maine, boasting…