In the face of elevated stock market volatility, rising US-China trade tensions, and plummeting bond yields, many are wondering whether these might be signs the United States is headed for a recession. Our analysis suggests the risk of recession is low in the near-term, but we thought now would be a good opportunity to look at why recessions matter, how we manage recession risk for our clients, and our current outlook for the S&P 500.

* * *

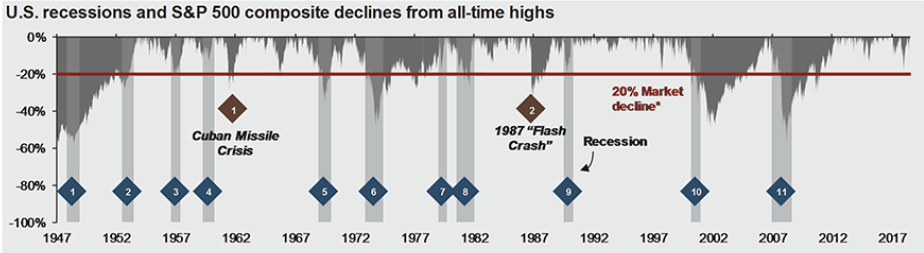

Historically, major bear market declines in the S&P 500, those of at least 40 percent, have occurred exclusively around US recessions. Thus, logic has it that if you can predict a recession then you can side-step a major portfolio drawdown.

Source: JP Morgan

Source: JP Morgan

Unfortunately, recessions are impossible to predict with consistency and accuracy, as demonstrated by economists’ abysmal track record of forecasting recessions. Recessions matter, but we recommend managing the associated risks, not predicting them.

We manage the risk of recession for our clients in three ways. First, in this low interest rate environment we recommend reserving up to three years of portfolio spending in a liquidity portfolio comprised of cash and short-term bonds. The combination of the liquidity portfolio and dividend income from the equity portfolio preserves the ability to spend through a recession without selling long-term equity holdings at depressed valuations. The liquidity portfolio also provides peace of mind, allowing clients to add excess cash to their equity portfolio in times of market distress.

Second, our equity investment process is centered on buying high quality companies that can pay and grow their dividends, and expand their competitive position, through the business cycle. Contrary to academic theory, we do not sacrifice long-term portfolio performance, vis-à-vis the S&P 500, by investing in these “conservative” companies. This allows us to protect client capital in recessions and participate in the market rebound that inevitably follows.

Third, we manage our clients’ equity exposure, within policy guidelines, using a weight-of-the-evidence market outlook framework. For example, if a client’s target equity exposure is 70 percent but the equity portfolio has grown to 80 percent, if the weight of the evidence suggests the outlook for equities is poor, we will rebalance the portfolio back to the 70 percent target.

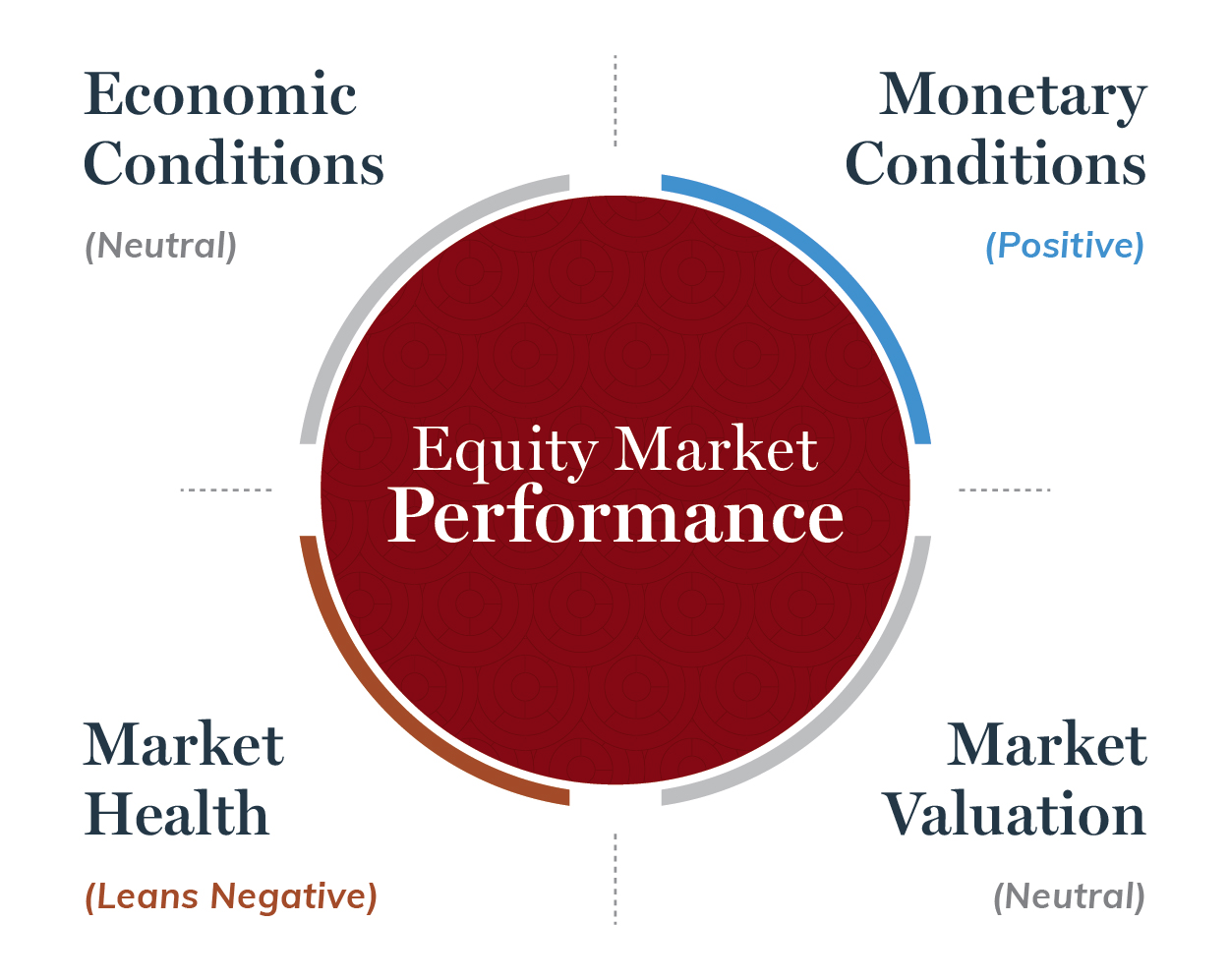

Our weight-of-the-evidence market outlook framework assesses the current state of four key pillars of equity market performance: economic conditions, monetary conditions, market valuation and market health. We rate each pillar as positive/leaning positive, neutral, or negative/leaning negative, then assign an aggregate rating to the market outlook.

Outlined in detail below, our current rating for the S&P 500 market outlook is neutral, with downside and upside risks approximately balanced.

Key to the S&P 500 market outlook is the state of the US economy. Historically, in the absence of a recession the US market tends to fall no more than 20 percent and bounces back quickly when it does. The quick 20 percent drop in the 4th quarter of 2018, and subsequent recovery, is a good case in point.

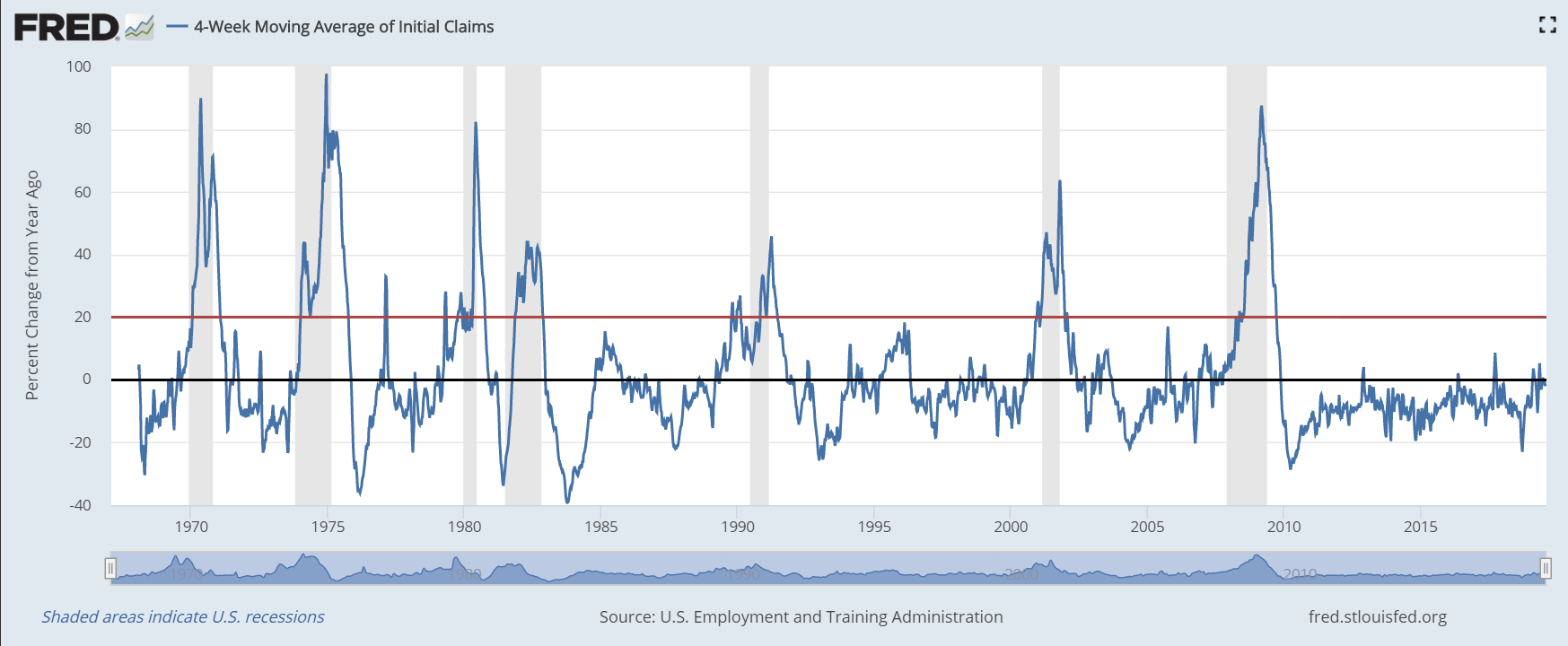

A key indicator we use to assess the health of the US economy is the 4-week moving average of initial jobless claims. Since World War II, no US recession has occurred without this indicator rising by 20 percent year-over-year early in the contraction. At present, it is falling year-over-year, indicating very little chance of recession in the near-term.

Nevertheless, we see downside risk to the US economic outlook stemming from the on-going global manufacturing downturn that began in early 2018. The escalation in US-China trade tensions has exacerbated the downturn, which now risks bleeding into the rest of the economy by depressing corporate and consumer confidence. The US economy continues to hold up on the back of strong consumer spending, but we are monitoring the downside risks closely.

We rate economic conditions as neutral.

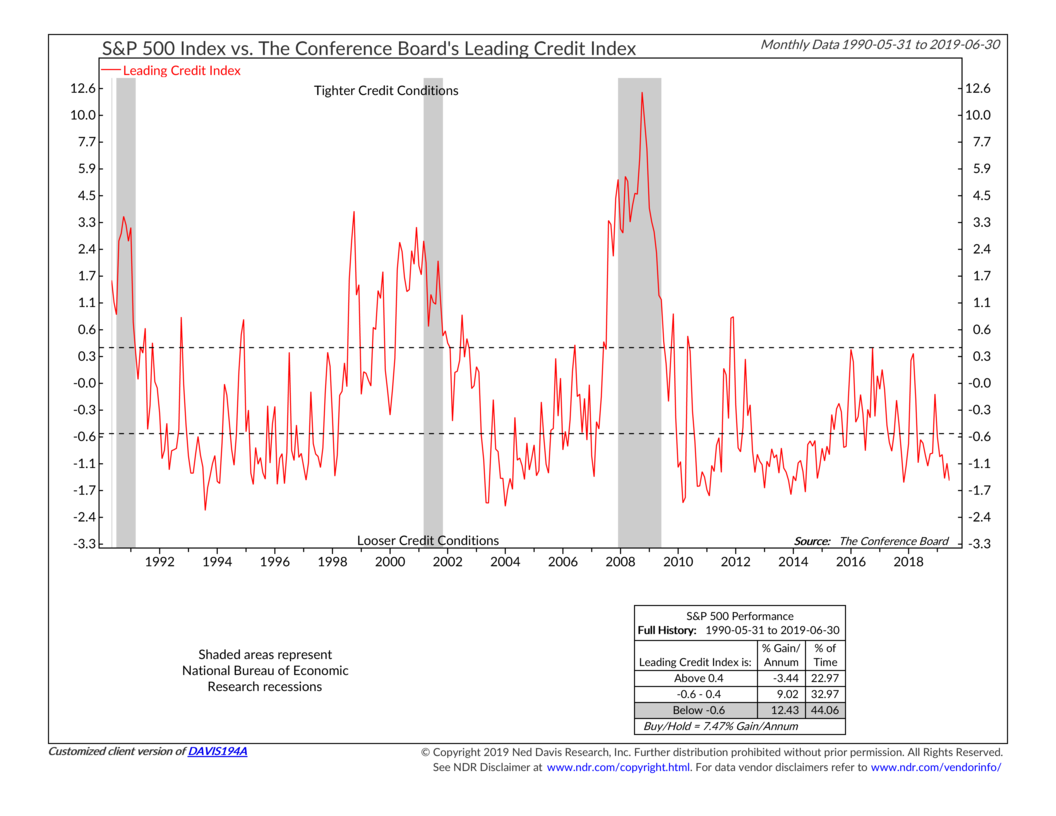

Credit is flowing freely throughout the economy for corporations and consumers, and central banks around the world are cutting interest rates in response to the global manufacturing downturn. This monetary backdrop acts as support to the economic outlook, and in turn equity valuations, leading us to a positive rating.

The positive monetary backdrop is demonstrated well by The Conference Board’s Leading Credit Index chart below. Historically, the S&P 500 has risen by more than 12 percent per annum with the index in its current configuration.

An age-old market axiom is “don’t fight the tape.” When the market is in a sustained and broad uptrend (i.e. healthy) or downtrend (i.e. unhealthy) it pays to respect the trend. Since late January 2018 the S&P 500 has been essentially trendless, returning just under 4 percent, including dividends.

The recent bout of market volatility has resulted in a wide swath of individual equities making new 52-week lows, a sign of deteriorating market health. Adding it all up, we rate the current health of the market as leaning negative.

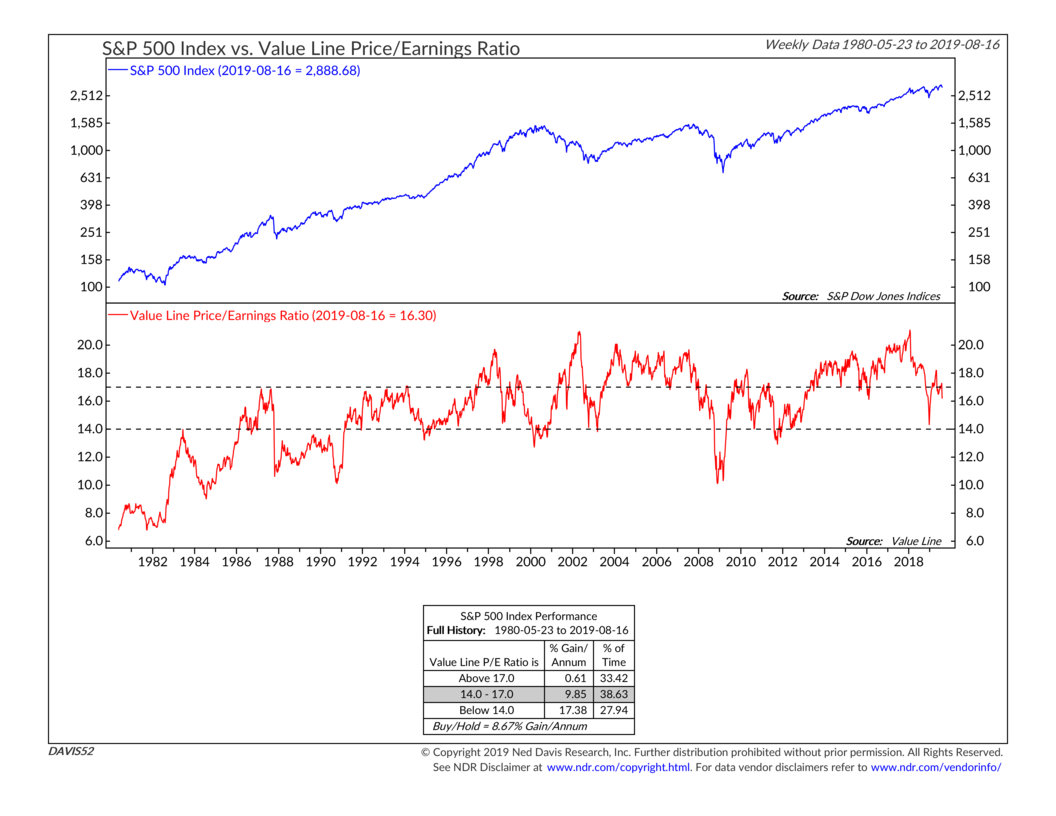

The S&P 500 appears moderately expensive relative to its own history, with a P/E multiple of just over 16 times versus an average range of 14-17 times (see chart below). Offsetting this modest overvaluation is the fact falling interest rates make dividend yields more attractive on a relative basis. We rate market valuation as neutral.

For as long as the current set of conditions remain in place, we believe the outlook for the S&P 500 is neutral. The key upside risk to our “neutral” rating is a US-China trade truce that would probably arrest the global manufacturing downturn; while the key downside risk is further deterioration in market health.

* * *

With strong US economic momentum and an extremely accommodative monetary backdrop, we believe the risk of outright recession in the US is very low over the next 12 months. In our portfolios, we shall continue to control and manage the risks that we can by hewing to high-quality equities of companies able to generate plenty of free cash flow and grow dividends. The market will exhibit its normal ups and downs; but, with no sign of recession directly ahead, market dips should be moderate and short-lived.

Maine Huts & Trails provides outdoor excursions in beautiful Western Maine, boasting…

Buy low and sell high. It’s a simple concept and one of…